Picking a Credit Card

In our previous blog post, we went into the abstract concepts and implications of credit cards on credit scores. This post’s focus is on the tangible benefits that credit cards offer and how to select the right one for your lifestyle.

Benefits of Credit Cards

Credit cards offer concrete benefits apart from their role in building credit. These perks include the following and more:

- Price matching on purchases

- Extended warranty periods

- Purchase protection against theft or fraud1

- Travel benefits

- Exclusive cardholder privileges

- Percentage based cashback / point accrual

Benefits are offered by credit card companies for free as an incentive to attract customers in a competitive credit card market. Essentially, these companies want to lend money so that they can earn interest on late payments. Ultimately, credit card companies expect that the interest collected from late credit card balances will outweigh the expenses incurred from providing these benefits.

Knowing this, it’s essential to maintain responsible credit card usage. Earning 2-3% cashback in rewards doesn’t matter if you’re paying interest at an annual APR rate of 20-30%.

Credit Cards Tiers

Credit cards suit diverse spending habits and individuals, providing varying benefit levels. Notably, certain cards entail an annual fee, offering extensive perks in return. Recognizing these distinct tiers —beginner, standard, and premium— is important for choosing a card that aligns with your requirements.

Beginner Cards

Overview: Credit building, poor benefits, tailored for new spenders

Annual Fee: None

Beginner cards offer minimal cashback rates and little to no features. They target individuals with limited or no credit history, focusing on establishing credit. Some beginner cards may require a security deposit or a guarantor to minimize the lender’s risk.

Standard Credit Cards

Overview: Credit building, decent cashback, daily expenses

Annual Fee: None - Low

These cards are standard, generally no-annual-fee offerings. Typically, they offer decent cashback percentages rates based on what you spend.

High End Credit Cards

Overview: excellent travel perks, daily expenses, heavy spenders

Annual Fee: Med - High

Tailored for individuals with a established credit history, high-end cards offer premium benefits especially for travelers. Instead of cashback, they accumulate points redeemable for discounted flight prices, catering to frequent travelers and offering significant travel-related perks like TSA precheck and airport lounge access.

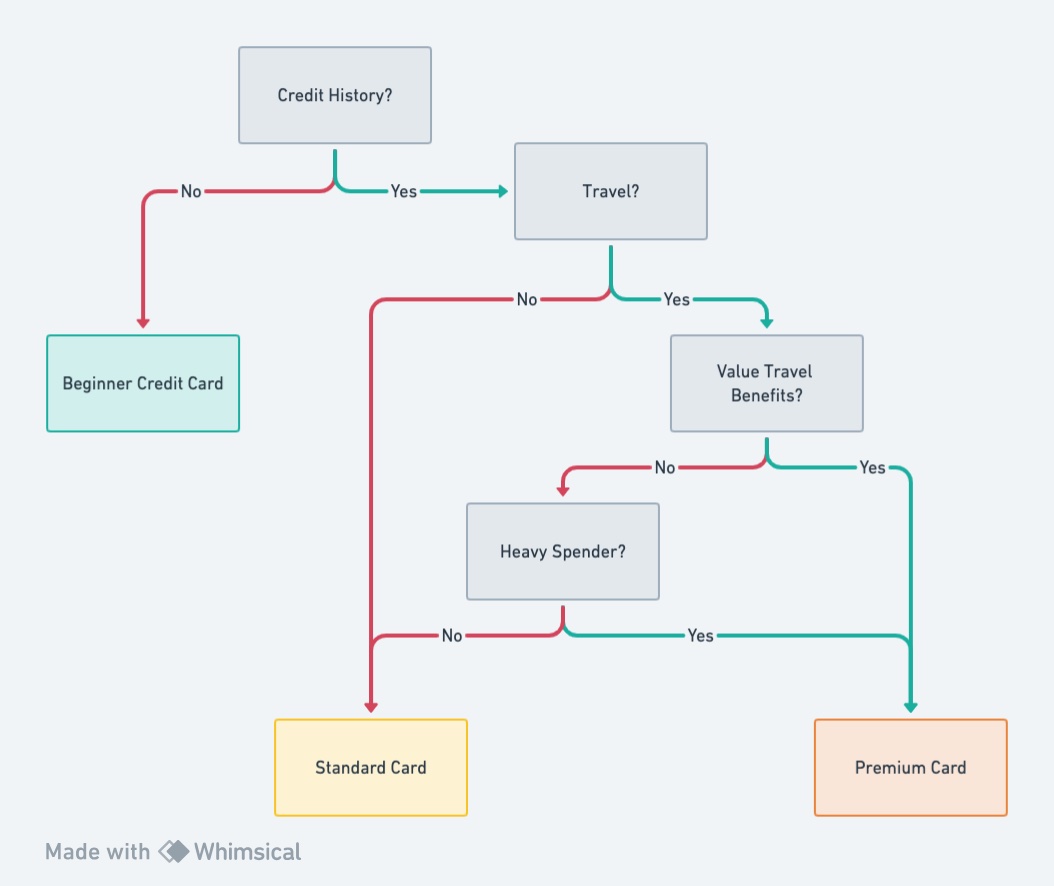

Finding Your Ideal Credit Card

A visual flow chart guide:

Assessing Benefits

Many cards provide standard fringe benefits such as fraud protection, price matching, and extended warranty/return periods, typically associated with Mastercard, Visa, and American Express (AMEX) cards. Ensuring your card includes these basics is crucial before exploring further benefits.

Once standard benefits are confirmed, consider these factors:

- Do you have credit history?

- Is frequent travel part of your lifestyle?

- What’s your annual spending?

- How does your spending break down by category?

Little to No Credit History

Opt for a Beginner Credit Card and Plan for Future Upgrades

For starters, prioritize building good credit habits with any basic/beginner credit card. Since rewards on beginner cards are minimal and you’ll likely upgrade later, focus on responsible use. Optimizing at this step while rewards are poor and while you’re likely not spending a lot is a waste of time since you’ll upgrade to a better credit card anyways.

Infrequent / Occasional Traveler

Choose a No Annual Fee Standard Card

If travel isn’t super frequent, avoid premium cards. The benefits of premium cards, mostly revolving around travel perks, won’t hold value without frequent travel.

Frequent Traveler

It depends on how much you value travel benefits and how much you spend annually

The decision to opt for a premium card hinges on your valuation of travel benefits and your annual spending habits. To properly evaluate this, you should consider how much you would pay for the travel benefits provided by your card. Let’s call this dollar amount travel_benefit_cost.

Now Consider your annual spending. Typically, a premium card yields an additional 1-2% return for each dollar spent in specific categories compared to a standard card.

For the annual fee to be justifiable then the following equation should be true consistently.

annual fee <= travel_benefits_value + 1-2% * annual_spend.

So if you value the travel benefits highly or if you spend a lot, then you can probably justify a premium travel credit card.

Evaluating Personal Spending Categories

After pinpointing the card tier that suits your needs, assess your spending across various categories to select a card offering decent cashback rates.

For standard cards, aim for a minimum of 3% cashback in your primary spending categories. Ideally, you’ll find this rate applicable to multiple categories. Premium cards typically excel in dining and travel-related purchases, offering higher rates of 4 - 5%.

Leveraging Multiple Cards

To optimize credit card benefits, consider acquiring multiple cards to cover diverse spending categories. Some cards offer high cashback rates in specific categories but lower rates in others2. By strategically selecting cards based on their strengths, such as one for groceries and another for dining, you can maximize cashback rewards.

There are specialized cards tailored to specific spending categories like the Chase Flex with a rotating 5% cashback category or Bylt offering cashback on rent payments. Collecting such cards enables broader coverage across various spending categories.

Owning multiple cards has additional advantages. It allows you to stack sign-up bonus offers and offers more credit lines to expedite building a credit history. However, having numerous credit lines might increase risk perception by lenders. Furthermore, irresponsible usage could lead to debt accumulation and substantial interest payments.

Summary

This is a huge read, but credit card selection takes a while to reason through, but it’s not too bad once you get the basics down! Thanks for reading! Yes I realize I’m a nerd.

-

If you think about it, credit card companies only offer fraud protection because fraudulent credit card use involves the company’s money rather than yours (since they’re lending to you!), making the company more motivated to track and recover the funds. This is why debit cards don’t have nearly the same protection as credit cards. ↩

-

Credit card companies have to maintain sustainable benefits against interest payments. They can’t offer high cashback rates in all categories without incurring losses. Balancing higher rates in specific categories with lower rates in others is their strategy to ensure a sustainable benefit structure from a business perspective. I’m confident that if you looked at all credit cards and looked at how much cashback rewards they paid out to cardholders, they’d converge on similar numbers. Pay too much in rewards and you lose money as a business. Pay too little in rewards, and you don’t attract enough customers to collect interest payments from. ↩